Just a tiny bit bearish here, but looking for a range and possible vol expansion.

Buy to open SPX Jul/Aug 1900 put calendar for 12.00 or lower.

Now this may look like the breakevens on this trade are reallllly tight.

And they are. But there are some other things to consider.

We are buying an implied volatility of around 12%. That’s pretty low. If the volatility expands, then our breakevens expand.

A move to 1930 or 1860 and we will add to the trade. The way the market is trending, we’ll probably be adding to the upside very soon.

Update: June 5th, 2014

1930 was hit today on the rally from the ECB voodoo, so we are going to add our second round.

Buy to open Jul/Aug 1940 call calendar for 9.80 or lower (mid is 9.60).

A move to 1952 will put me into the third set of calendars

Update: June 23rd, 2014

The move higher is continuing… normally I would look to add to this trade, but instead I will close out the lower calendar and “roll” it up to a higher strike.

Here are the greeks before the adjustment:

D: -30 G: -.55 T: 17.50 V: 427

Here is the adjustment:

Sell to close SPX Jul/Aug 1900 Call calendar at 8.90 or higher

Buy to open SPX Jul/Aug 1965 Call Calendar at 9.70 or lower

Greeks after:

D: -10 G: -1.24 T: 27.88 V: 391.41

Basically, this adjustment helps to reduce our directional exposure and gives us a little kick higher with theta. We will also be selling a calendar that has an IV of 12% and buying a calendar that has an IV of 8%, so if vol rises our new calendars will benefit a little better.

1975 puts me into another add.

Update – July 3rd, 2014

With the continued rip higher, we’re now in damage control mode, looking to reduce the overall risk in the trade with much lower odds of profitability.

What we will do here is roll up the 1940 call calendar higher:

Sell to close Jul/Aug 1940 put calendar for 6.30

Buy to open Jul/Aug 1980 put calendar for 10.20

This will cut our directional exposure in half and double our theta– but we’re now trying to work the trade back to breakeven.

The reason this trade isn’t working out is because the implied volatility in SPX kept falling– we’re now buying the 1980 calendar with an IV of 7%!

That means if the VIX does pop here, we’ll make some of the losses back, on top of the theta gains.

Update: July 15th, 2014

Trade is doing much better… a little change in the implied volatility term structure, a pop in the VIX and a touch of theta has this trade profitable (finally).

With only 3 days left, it’s best to either run a stop where if you go from profits to breakeven close out… and make sure to close out by Wednesday at the close.

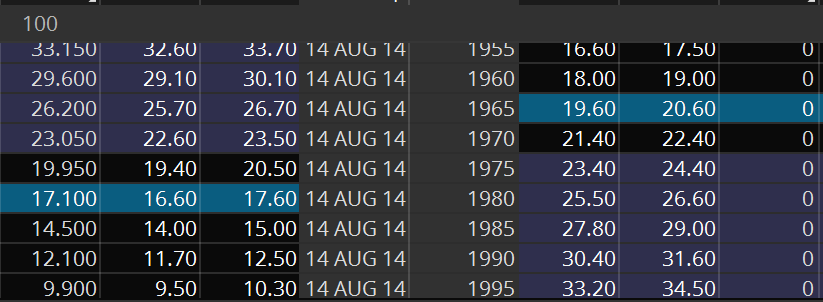

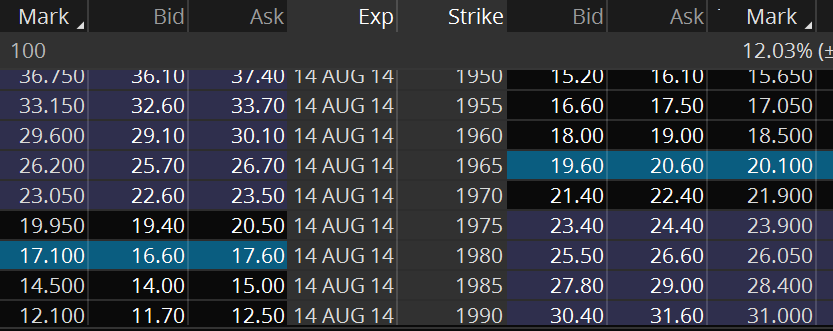

Aug Prices:

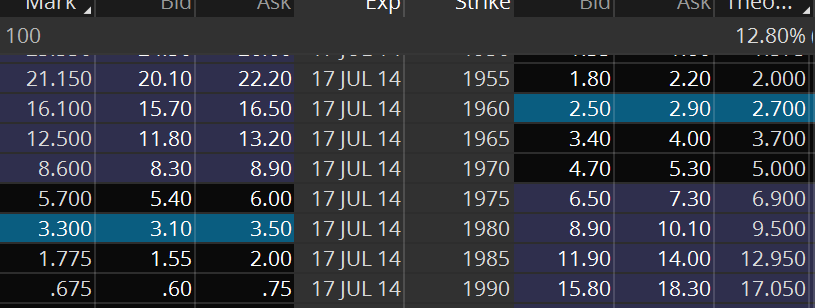

Jul Prices:

Calendar Close #1:

Buy To Close SPX Jul 1965 put @3.70

Sell To Close SPX Aug 1965 put @20.10

Total Price: 16.40

Calendar Close #2:

Buy to Close SPX Jul 1980 Call @3.30

Sell to Close SPX Aug 1980 Call @17.10

Total Price: 13.80

Margin and P/L

Calendar #1: 12.00

Calendar #2: 9.80

Roll From 1900 to 1965: 80

Roll From 1940 to 1980: 390

Total Margin: 2650

P/L Calculation

Calendar #1:

Jul/Aug 1900 Put Calendar

Enter at 12.00

Exit at 8.90

Loss: -310

Calendar #2:

Jul/Aug 1940 Call Calendar

Enter at 9.80

Exit at 6.30

Loss: -350

Calendar #3:

Jul/Aug 1965 Put Calendar

Enter at 9.70

Exit at 16.40

Profit: +670

Calendar #4:

Jul/Aug 1980 Call Calendar

Enter at 10.20

Exit at 13.80

Profit: +360

Total Profit: 370

Return on Risk: 14%