Home › Forums › Open Trades › Scaling Calendar in AAPL › Reply To: Scaling Calendar in AAPL

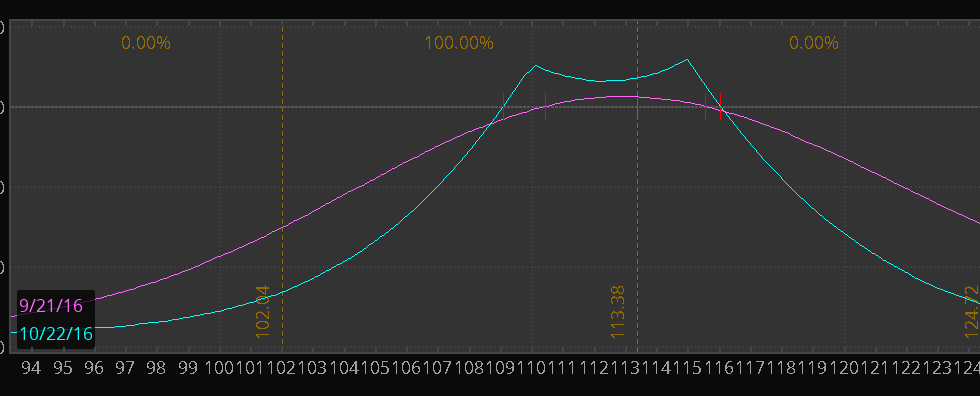

Here’s what the trade looks like right now:

Again, this looks like terrible risk/reward because the “tent” of the calendars is so low.

But let’s look at the extrinsic value of the options… we’re going to combine each strike and just separate the duration:

Oct 115 + 110 extrinsic: 3.06

Nov 115 + 110 extrinsic: 6.98

Now here’s the thing… the analytics assume that theta will decay “normally”. The current greeks assume that the theta on both option durations will be the same.

But it’s not the case!

The oct options have an IV of 18%

The nov options have an IV of 25%

Because of earnings.

The Nov options will decay at a much slower rate on an absolute basis compared to the Oct options.

Because the Oct options don’t have earnings in the cycle.

So headed into the next few weeks, we should see the curve continue to improve compared to what it appears on the analytics software.