At IncomeLab, our edge is found through understanding one thing:

The options market tends to overprice risk.

The fancy term for this is “consistent risk premium.”

Basically, we are net option sellers.

Yet unlike many option sellers out there, we don’t “set and forget” trades. Often times, they require active risk management, or we just get out of the trade for a loss.

The risk management is what sets us apart. We know our edge will be there as long as we don’t let a few trades get away from us.

We will talk about our trade recipes, but if these seem confusing, they are a lot simpler to understand by going and looking at our past trades to see how they worked out.

Download the trade recipes PDF here.

With that in mind, let’s talk about the primary strategies we trade at IncomeLab.

ICBase

Asset: SPX

Type: Iron Condor, Systematic

Market Outlook: Neutral

Trade Selection

- Go 60 days out in time.

- Look for a 10-wide put spread that offers a 9% return on risk (.80c-.90c credit per spread)

- Look for a 10-wide call spread that offers a 9% return on risk. (.80c-.90c credit per spread)

Trade Exit

Our goal is to remove the trade after capturing 50% of the credit in a 30 day timeframe.

If we can get profits out faster, we will. This will only happen if the VIX drops hard.

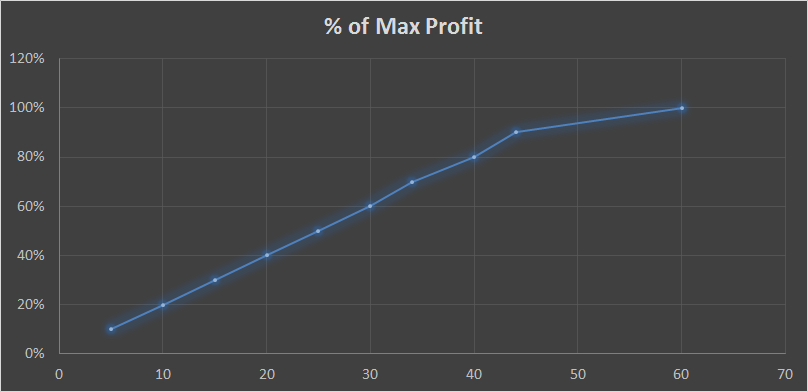

The picture below is a good guideline of what to look for in terms of profits relative to time in trade:

The sweet spot is at 30 days to expiration.

If you can capture 50% of maximum credit with 30 days left to expiration, that’s a good exit.

If you can capture 20% of maximum credit after being in the trade for only 10 days, that’s also a good exit.

The goal here is to maximize returns and minimizing time in the market.

Trade Adjustment #1

We will adjust the trade if either the short call or short put has a delta of 20-25. We are looking at an INDIVIDUAL OPTION DELTA here.

So, for example, if you have a 1790/1800 2030/2040 iron condor, if either the 1800 or 2030 option has a delta of 20-25, it’s time to adjust.

If our alert triggers, then we will buy options.

We will go 45 days out and select an option between 8-15 delta.

Our sizing on the calls is a function of the NET DELTA of the entire option position.

Our goal of the adjustment is to remove 50-65% of our NET DELTA exposure. For example, if our NET DELTA of an Iron Condor is -40 then we need to add 20-25 delta to bring our NET DELTA down from -40 to -15 -20 range. We’ll look to buy (2) 10 delta calls or (3) 8 delta calls for a total of +20 to +25.

If you are trading smaller size, then use index ETF options to hedge.

Trade Adjustment #2

If the market continues to move against us… normally another 30 points higher or 50 points lower and short strike’s delta goes to 30… then we will do a few things.

- Close out the hedge for a profit.

- Roll the losing spread out.

- Roll the winning spread in.

For example, say the market rallies hard. You buy a call to hedge. Then the market goes even higher. You would:

- Close out the call hedge for profits

- Roll the call spread higher

- Roll the put spread higher

The opposite is done in a market selloff. You would buy puts, and if the market sells off more you would:

- Close out the put hedge for profits

- Roll the put spread lower

- Roll the call spread lower

ICPlus

Asset: SPX

Type: Iron Condor, Discretionary

Market Outlook: Bearish

Trade Entry

Duration: 45 Days

28 Delta on the Short Calls

30 Delta on the Short Puts

10 Wide Spread

Target Credit: 5.00 – 5.30

Trade Exit

Profit Target of 20% of Credit Per Condor. For example, if credit received was $5.20 then our Profit Target is $1.00-$1.05. We’ll look to close this Iron Condor for $4.20 debit (5.20-1.00)

HARD STOP of -20% of Credit Per Condor. For example, if credit received was $5.20 then our Stop Loss is a drawdown of about $1.00-$1.05. We’ll look to close this Iron Condor for $6.20 debit (5.20+1.00)

EIP

Asset: RUT

Type: Unbalanced Butterfly, Discretionary

Market Outlook: Bullish

Trade Entry

Short Strike of the butterfly 20 points under current RUT Price

Low Strike 50 points under short strike

High Strike 30 points above short strike

So if RUT is trading at 1400, then your short strike would be 1380, your low strike 1330 and your high strike 1410.

Adjustment #1:

If RUT Trades higher than the upper strike, add to the trade (Tier 2)… same structure but higher strikes.

Adjustment #2:

If RUT Trades higher than the upper strike, add to the trade (Tier 3)… same structure but higher strikes

Exits

If Only Tier 1 On, Profit Target is $400 per spread, Hard Stop is -$400 per spread

If Tier 1 and Tier 2, Profit Target is $800 per spread, Hard Stop is -$800 per spread

If Tier 1 and Tier 2 and Tier 3, Profit Target is $1200 per spread, Hard Stop is -$1200 per spread

KISS CONDOR

Asset: SPX

Type: Iron Condor, Systematic

Market Outlook: Neutral

Trade Entry

Duration: 30 days out

Profit Target: 70-80% of Credit per Iron Condor. For example, if Credit was .80c per Iron Condor, we’ll collect .60c and exit for a .20c debit.

Stop Loss: -2X Profit Target per Iron Condor. For example, if Credit was .80c per Iron Condor, and our Profit Target is .60c, we’ll close if this trade is down $1.20