Home › Forums › Market Discussion › Delta hedging for common trade setups

- This topic has 9 replies, 5 voices, and was last updated 7 years, 2 months ago by

Suresh.

-

AuthorPosts

-

March 16, 2016 at 11:55 pm #5029

Colin

ParticipantCan you go over some of the theory behind why adjusting trades using deltas is effective? Perhaps you could touch on how to calculate the current delta for some of your more common trades such as iron condors, butterflies, or any other ones where it is typically used. Also can you comment on how much delta you like to remove from each of the different types of trades and when is an appropriate time to put the hedges on.

March 17, 2016 at 8:56 am #5031Steven Place

KeymasterWith income trading you are not betting on the direction of where a market will go.

Instead you are betting that the premium offered is higher than the risk you can receive.

So when you put these kinds of trades on, your profit comes from the premium decay over time.

That’s your reward.

What’s your risk?

Well, in a normal trade, let’s say long 100 shares of AAPL… your risk is on a selloff.

This technically is delta risk. Option traders just like to assign names to things to confuse people. Delta = directional risk.

And on this long stock example your reward also comes through delta… this time to the upside.

With income trades your reward comes from theta. Decay of that options premium. That’s your reward.

Your risk? Directional movement both to the upside and downside.

And because this is an options trade, that delta can changes as a function of time (charm) and price (gamma).

When you manage risk in a long stock scenario, you use stops. Basically if your risk gets too high, you remove your deltas by closing out the position.

With income trades, you also remove deltas, but you are doing it in a more complex way.

The best phrase I have for this is:

MANAGE YOUR DELTAS UNTIL THE THETA KICKS IN

Now… to calculate your entire position delta, there’s a couple ways you can do it.

The first way is just to take the delta of each option and your total size and add them all up.

Option greeks are aggregate in nature, so you can just use a calculator.

Let’s take an example of a bull put spread.

Selling a 30 delta put

Buying a 20 delta put

So your net delta is 30 – 20 = 10.

Your equivalent delta is going to be 10 shares of stock.

Now things do get more complicated, that is why we have analysis software.

In thinkorswim, you use the analyze tab to figure out your net delta in a position:

Deciding When to Hedge

This is going to be different depending on what school of thought you belong to. There’s no right or wrong answer and they tend to overlap.

1. Delta band trading. You have an acceptable level of directional risk you’re willing to take on a trade and once it breaches that you remove some of the deltas.

You can see this really well if you just look at a short straddle. At first your delta on a short straddle is 0 but it can go all the way up to 100. So maybe when your delta reaches 30 you adjust the trade.

2. Delta/Theta ratios. This is a pure risk/reward equation. If your directional risk isn’t justified by the time decay you are receiving then you need to bail. A good D/T ratio to start with is 1.5.

3. Price levels. If a key technical level in the market is violated, then adjust the trade.

4. Single option delta. If the delta on one of your short options of an iron condor reaches 20, then adjust the trade.

There’s probably other techniques I’ve missed but they all have the same kind of idea– at some point your risk gets too high and you need to modify the trade so you don’t get blown out of the water.

As for me personally, it’s going to depend. With adjustment levels I have some guidelines but I also look at charts to see if my adjustment levels are too obvious. Nothing is more frustrating to adjust a trade only to see reversion finally kick in.

With iron condors, I set price levels as a function of max delta / 2. So when I initialize the trade I look at my max delta, say 100, and I look for the price level where my delta hits 50. You can use analytics software to do that.

With calendars and butterflies, I believe it’s easier to utilize a scaling technique compared to try and modify deltas aggressively. Obviously there are exceptions but I think slowly scaling into a position will leave you better off compared to going full size and losing the “high ground” in a trade.

Let me know if you have any questions about this.

March 17, 2016 at 9:17 am #5032Suresh

ParticipantWhy do you use VXX puts for upside risk. I know the UL will drop in value as we rip higher. So buying puts makes sense to manage the upside risk. But how to calculate deltas when using VXX to remove the short bear call spread delta. esp. when using indices as SPX/ SPY. In the RUT put fly you used IWM to cut deltas since IWM is 1/10th of RUT. But VXX is not related entirely to SPX/SPY/RUT.

March 17, 2016 at 9:45 am #5034Marco

ParticipantSuresh you can use the porftolio beta weight of think or swim. Or, if you are a math dude, you can calculate it. 10 delta on something that costs you 200 bucks is like 100 delta on something that costs you 20 bucks, without taking volatility in account (and i don’t know if TOS does that for you).

EDIT Steven just to clarify: what does it mean “max delta”? The delta you would have at the breakeven point of the IC today?

-

This reply was modified 7 years, 2 months ago by

Marco.

March 17, 2016 at 11:57 am #5037ParticipantThanks Marco. I know VIX “basically” tracks the volatility of S&P 500. However, vix can be in backwardation for a long time (even though the price action in SPX may not correlate truly) and using an instrument that is a derivative of VIX may be “insufficient”. Let me know if my thinking is incorrect.

March 17, 2016 at 12:01 pm #5038ParticipantHere is my idea on using vxx puts to hedge on the upside: they should work better than spy/spx calls cause

1) vxx is an etf that track futures. Like every etf suffers of rollover costs. I don’t know if the spy is just a bunch of stocks or tracks the ES.

2) vxx tracks something that has an embedded reversion to the mean nature. So, on a very long run, it’s gonna go to 0March 17, 2016 at 1:22 pm #5042ParticipantThanks Marco. That’s useful info.

March 17, 2016 at 7:58 pm #5046Cody

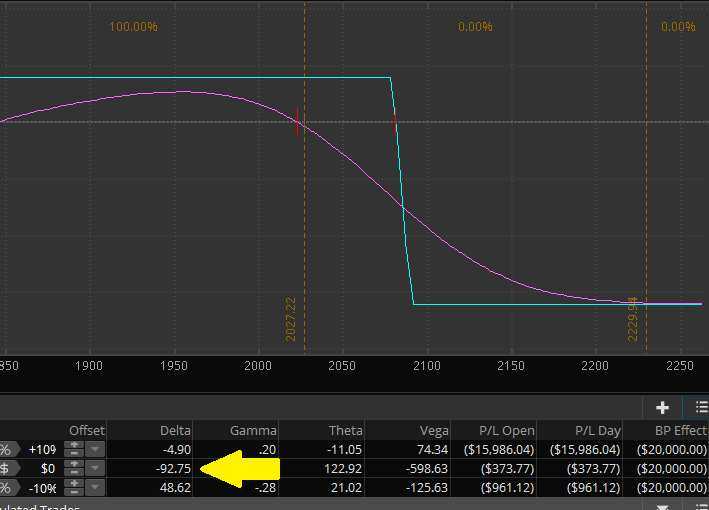

ParticipantI want to expand on or I guess be more specific on Marco’s question above about “max delta” for delta band adjustment technique because I’ve wondered the same. As an example, if I’m modeling an IC in TOS and I switch the mode from P&L to delta, and then day step +4, it becomes obvious that “max delta” will vary depending on time in the trade (and I suppose this is just a visualization of charm). But when you are just entering a trade and looking for that “max delta” figure to divide by 2, are you using the max today at entry? In 2 weeks? In 30 days?

March 18, 2016 at 6:29 am #5047ParticipantGonna add this regarding vxx hedging:

March 18, 2016 at 8:58 am #5048ParticipantAh. I see now why buying VXX puts is a better hedge than straight calls more often. Thanks again Marco.

-

This reply was modified 7 years, 2 months ago by

-

AuthorPosts

- You must be logged in to reply to this topic.