Quick Notes (10/27/17)

It’s been two weeks but none of the premium has come out of the options… what gives?

The answer is this:

There are two parts to the risk premium of an option: time, and volatility.

In this case, the time premium has come out of the options, but it has been replaced by volatility premium.

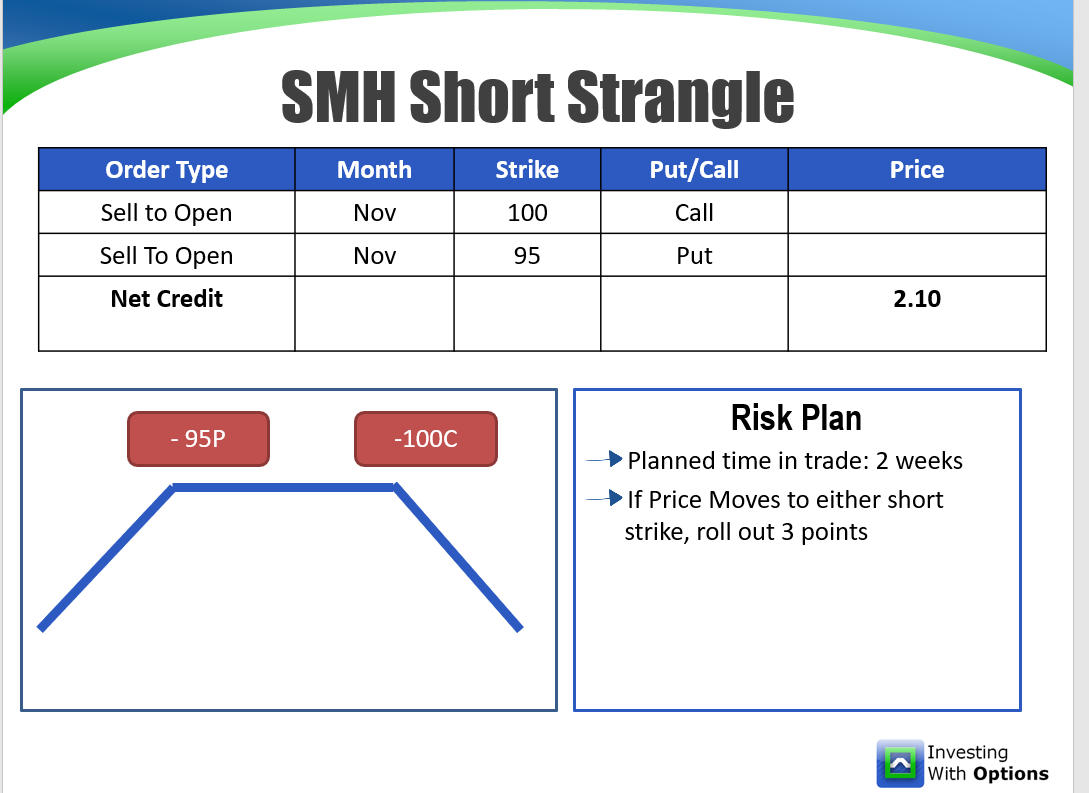

When the trade was put on, the 95 put had an implied volatility of 20.18%. It now sits at 25%.

The 100 call had an implied volatility of 16.44%. It’s currently at 17.78%.

So what gives? Why has implied vol cranked up? Well, there were a lot of earnings in the semiconductor space. More specifically, INTC, which had 10% of the weighting in the ETF, had earnings.

In the next few trading days, we *should* start to see implied volatility come out as earnings risk no longer exists. When that happens, the strangle will be performing much better.

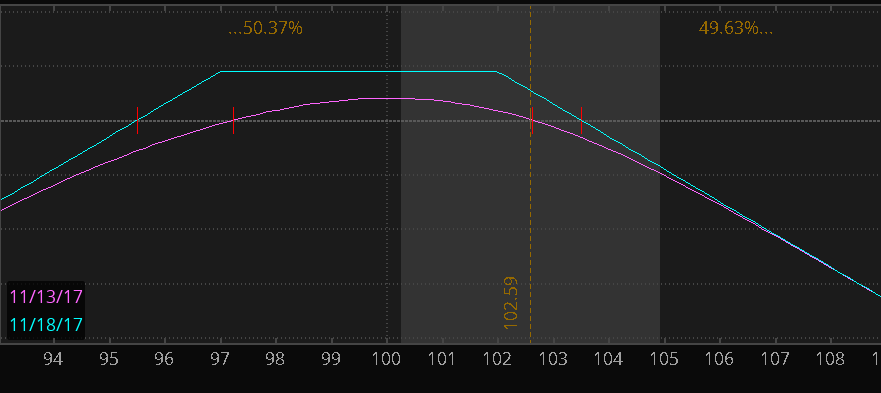

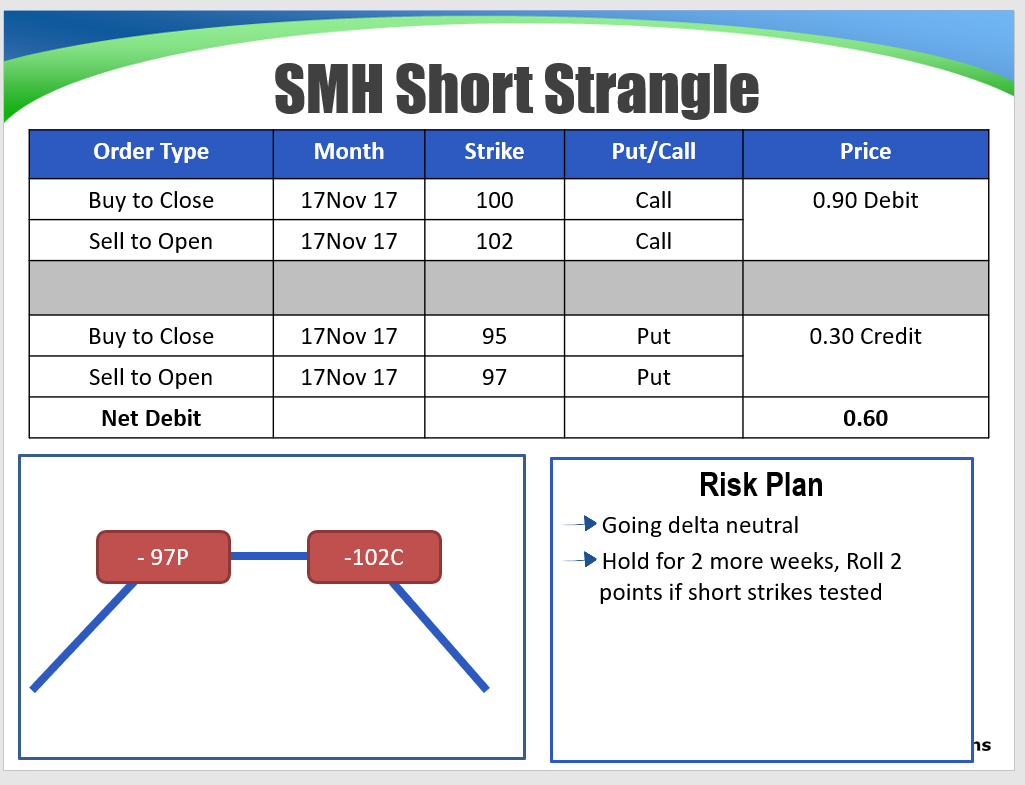

Update: 10/27/17

Going to roll the entire strangle higher to remove directional risk and increase available theta profits.

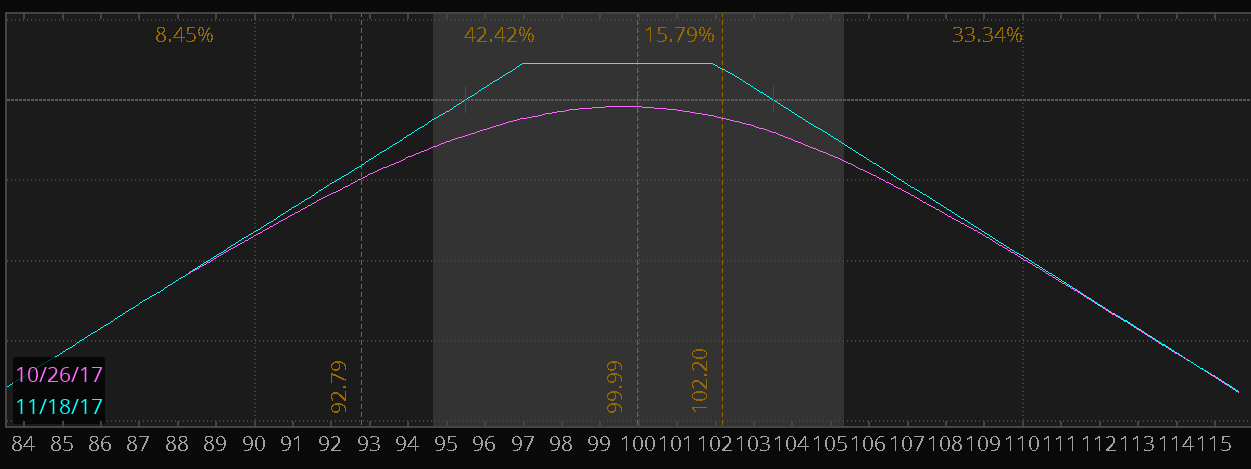

Update – 11/15/17

Closing out the trade at breakeven.

Buy to Close SMH 102 Call for 1.10. Let the 97 Put expire worthless.